Most companies budget headcount against base salary. That single decision is why expansion plans miss their numbers in year one, and why a EUR 75,000 engineer often costs the business closer to EUR 109,000 fully loaded. This guide breaks down the formula, the four cost components every employer pays, and what European companies need to budget when hiring into Vietnam.

TL;DR

- An employee costs a company 1.25x to 1.4x their base salary on average in developed markets, according to US Bureau of Labor Statistics. Base salary is typically 60 to 70 percent of total employer cost; the rest sits in statutory contributions, benefits, and overhead.

- Total employer cost has four components: direct compensation, employer taxes and statutory contributions, mandatory and competitive benefits, and indirect overhead. Missing any one of them produces a budget that breaks within 90 days.

- In Vietnam, mandatory employer contributions to Social, Health, and Unemployment Insurance sit at 21.5 percent of contractual salary before any benefit is added, making the fully loaded multiplier different from European markets. For a senior backend role, total cost in Vietnam typically lands 50 to 60 percent below the Netherlands equivalent.

Employee cost is the full amount a company pays to employ one person: base salary, employer statutory contributions, mandatory and competitive benefits, onboarding, and indirect overhead.

For budgeting, use fully loaded employee cost instead of gross salary. Gross salary tells you what the employee earns. Fully loaded cost tells you what the business must actually fund.

What does it actually cost a company to employ one person?

An employee typically costs a company between 1.25 and 1.4 times their base salary once statutory contributions, benefits, and overhead are added in. That figure comes from the US BLS Employer Costs for Employee Compensation series, which tracks the breakdown across roughly 380,000 employer observations.

The multiplier is a useful starting point. It is not a universal truth. The number swings 15 to 25 percent depending on country, industry, company size, and how compensation is structured between cash, equity, and benefits.

Below is the breakdown that explains where the gap between salary and total cost comes from, why the gap is wider for senior roles, and how to model the number for a market you are entering rather than one you already operate in.

Where the 1.25x to 1.4x rule comes from (and when it breaks)

In US BLS data for Q2 2025, wages and salaries averaged 70.2 percent of total employer compensation. Benefits accounted for the remaining 29.8 percent. The implied multiplier on base pay: 1.42x.

The rule under-predicts in three contexts:

- High-benefit markets in Western Europe where statutory employer contributions and mandated benefits push the multiplier closer to 1.5x to 1.55x.

- Regulated industries (finance, pharma, energy) where compliance and certification overhead loads 8 to 15 percent extra onto each role.

- Small companies under 50 employees, where overhead per head is structurally higher because fixed costs spread thinly.

The rule over-predicts when a meaningful share of the workforce is contractor or platform-based, where statutory employer contributions do not apply in the same way.

Why base salary is the wrong number to budget against

A common pattern: a European CFO budgets a new market entry at EUR 60,000 per engineer based on local salary survey data. The first six months come in at EUR 78,000 to EUR 84,000 per engineer once contributions, benefits, equipment, and onboarding amortisation are added.

The forecast was not wrong on salary. The forecast missed everything else.

Companies that survive the market entry budget against fully loaded costs from day one. Companies that miss their year one numbers usually budgeted against base. To understand how this connects to the upstream hiring spend, the breakdown of recruitment cost shows the parallel pattern where time-to-fill and agency fees compound on top of salary, not separately from it.

The 4 cost components every employer pays (whether they track them or not)

Total employer cost breaks into four categories. Each one carries a typical share of the total, and each one has a line item that internal forecasts most often miss. The order below tracks how the components show up on a payroll register, from largest to smallest share.

1. Direct compensation: salary, overtime, commission, and bonuses

Direct compensation is typically 60 to 70 percent of total employer cost. It covers base salary, overtime pay, sales commission, performance bonus, and the 13th month payment where standard (Vietnam, the Philippines, much of Latin America).

The line CFOs miss most often: accrued bonus and unpaid commission that have not been disbursed yet but are already a liability. A USD 60,000 base salary role with a 15 percent target bonus carries USD 9,000 in accrued bonus by year end whether or not the cash has moved.

Treat accrued variable pay as part of cost from the start. It avoids the recurring Q4 surprise where finance forecasts payroll one number and reality lands 10 to 15 percent higher.

2. Employer taxes and statutory contributions

This is the line that surprises foreign employers most. Statutory employer contributions range from roughly 7.65 percent (US FICA employer share) to above 30 percent in parts of Western Europe.

Three anchor points to memorise:

- United States: 7.65 percent FICA employer share (Social Security plus Medicare), plus state unemployment insurance that varies by state.

- Netherlands: roughly 17 percent employer charges (WAO/WIA disability, ZVW health, premiums for unemployment), capped at a salary ceiling.

- Vietnam: 21.5 percent mandatory employer contributions for Social Insurance, Health Insurance, and Unemployment Insurance, governed by Decision 595/QD-BHXH and the Law on Social Insurance.

Statutory contributions are not optional and not reducible through structuring. They are the fixed cost layer that sits on top of base salary in every market. The Vietnam tax system guide breaks down the full schedule including PIT progressive bands and how contributions interact with personal income tax on the employee side.

3. Mandatory and competitive benefits

Benefits split into two categories: legally required and competitive.

Legally required benefits include public or private health coverage (mandatory in most EU markets), social insurance (mandatory everywhere), and statutory leave entitlements (paid vacation, sick leave, parental leave). The BLS Employer Costs series shows benefits averaging 8 to 12 percent of total cost in the US, with Eurostat data putting the figure closer to 15 to 22 percent in Western Europe.

Competitive benefits are what the employer adds to win and retain. Private health upgrade, pension top-up beyond statutory, equipment stipend, learning budget, and stock options. The mix matters more than the headline number. A strong employee benefits package can substitute for 5 to 10 percent of base salary in retention impact when the package is designed around what the workforce actually values.

4. Indirect overhead: workspace, equipment, training, management time

Indirect overhead is the hardest category to quantify, and the one most underbudgeted. It typically runs 8 to 15 percent of total cost for office-based roles and 6 to 10 percent for remote roles.

The four line items inside indirect overhead:

- Workspace and equipment: USD 1,500 to USD 3,500 setup per remote engineer, then USD 200 to USD 400 monthly for tools, software licences, and internet stipend.

- Training and development: Training Magazine 2024 Training Industry Report puts the US average at roughly USD 1,300 per employee per year. Tech and finance employers typically spend two to three times that.

- Management time: 1 manager per 7 to 10 reports means 10 to 14 percent of a manager’s salary loads onto each direct report. Treat this as an estimate, not a precise figure.

- Onboarding amortisation: the first 90 days of a new hire are typically 40 to 60 percent productive. The lost productivity is a real cost, just one that does not appear on a payroll register.

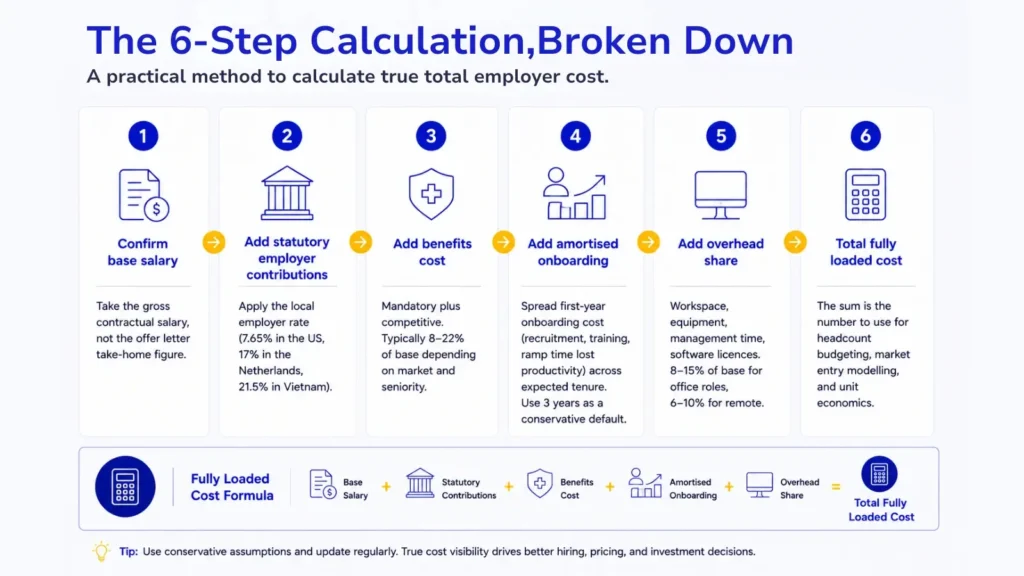

How to calculate fully loaded employee cost (6 Steps)

The fully loaded cost formula combines the four components into a single number. The version below works in any market, in any currency. The variable is which percentages apply where.

Fully loaded employee cost = Base salary + Employer statutory contributions + Benefits + Onboarding (amortised) + Indirect overhead

The 6-step calculation, broken down

- Step 1. Confirm base salary: Take the gross contractual salary, not the offer letter take-home figure.

- Step 2. Add statutory employer contributions: Apply the local employer rate (7.65 percent in the US, 17 percent in the Netherlands, 21.5 percent in Vietnam).

- Step 3. Add benefits cost: Mandatory plus competitive. Typically 8 to 22 percent of base depending on market and seniority.

- Step 4. Add amortised onboarding: Spread first-year onboarding cost (recruitment, training, ramp time lost productivity) across expected tenure. Use 3 years as a conservative default.

- Step 5. Add overhead share: Workspace, equipment, management time, software licences. 8 to 15 percent of base for office roles, 6 to 10 percent for remote.

- Step 6. Total fully loaded cost: The sum is the number to use for headcount budgeting, market entry modelling, and unit economics.

Worked example: USD 60,000 base salary, US-based engineer

| Cost component | Amount (USD) | % of total |

|---|---|---|

| Base salary | 60,000 | 74% |

| Statutory contributions (FICA 7.65%) | 4,590 | 6% |

| Benefits (12%) | 7,200 | 9% |

| Onboarding amortised | 2,500 | 3% |

| Indirect overhead | 6,500 | 8% |

| Fully loaded total | 80,790 | 100% |

The multiplier on this example: 1.35x. That lands within the BLS national average band.

Worked example: EUR 75,000 base salary, Dutch backend engineer

| Cost component | Amount (EUR) | % of total |

|---|---|---|

| Base salary | 75,000 | 69% |

| Statutory contributions (roughly 17%) | 12,750 | 12% |

| Benefits (15%) | 11,250 | 10% |

| Onboarding amortised | 3,000 | 3% |

| Indirect overhead | 7,000 | 6% |

| Fully loaded total | 109,000 | 100% |

The multiplier: 1.45x. That is the European average for technical roles. The Netherlands example sets up the Vietnam comparison in the next section, where the same role lands at a meaningfully different number.

The mechanics of converting these calculations into actual monthly payouts are covered in the payroll processing guide, including the operational steps where statutory contributions, benefits, and net pay reconcile against the contractual structure.

What drives the difference between a low-cost and a high-cost employer

Five variables move the multiplier. Knowing which ones apply to your situation predicts where your fully loaded cost will land before you run the math.

| Factor | Low end | High end | What pushes it |

|---|---|---|---|

| Country | 1.2x multiplier (US, Singapore) | 1.55x (France, Belgium) | Statutory employer contribution rate |

| Industry | 1.3x (tech, consumer) | 1.5x (finance, pharma, energy) | Compliance, licensing, certification overhead |

| Company size | 1.3x (over 1,000 staff) | 1.5x (under 50 staff) | Fixed overhead spreads thin or thick |

| Seniority level | 1.3x (mid-level) | 1.6x (director+, with equity) | Benefits and equity scale non-linearly |

| Employment model | Contractor: 1.05x | FTE: 1.4x, EOR: 1.25 to 1.35x | Where statutory and benefit cost sits |

Country: statutory contribution burden varies from 7% to 35%

The biggest single variable. The US sits at 7.65 percent employer FICA. Vietnam at 21.5 percent. Netherlands at 17 percent. France can exceed 30 percent. The same role in two countries can have a 20 percent cost difference before any benefit decision is made.

Industry: regulated sectors carry 8 to 15 percent compliance overhead

Finance and pharma require licensed roles, certification refreshes, and audit overhead. Each employee carries a compliance load that does not exist in unregulated industries. Plan for the line, do not discover it.

Company size: under-50 companies have the highest overhead per head

Office leases, HRIS subscriptions, insurance minimums, and management bandwidth all spread thin in small companies. A 30-person company pays a higher per-head overhead than a 3,000-person company on identical work.

Seniority: benefits and equity grants scale faster than base

At director level, equity grants, executive health plans, and signing bonuses can double the multiplier. A USD 200,000 director-level role can carry USD 320,000 to USD 360,000 fully loaded, where benefits and equity are tracked separately.

Employment model: FTE, contractor, and EOR shift where the cost sits

FTE absorbs all four cost components on the employer balance sheet. Contractor shifts statutory contribution and benefit cost to the worker (and creates misclassification risk if the relationship resembles employment). Employer of record (EOR) sits between the two: the EOR provider runs payroll, contributes statutory amounts, and provides benefits, charging a fee on top of the loaded cost.

Employee cost in Vietnam: what European companies need to budget

European companies entering Vietnam tend to model headcount cost using their home-market multiplier and apply it to local salary data. The result is a 15 to 25 percent error in either direction, because Vietnam statutory contributions, the 13th month payment, and the benefits expectation gap all break the home-market assumption.

This section covers the three numbers a European CFO needs to budget Vietnam correctly: the mandatory employer contribution rate, the equivalent role cost compared to the Netherlands, and the breakeven point between EOR and entity setup.

Vietnam mandatory employer contributions: 21.5 percent (the number to memorise)

Three contributions apply on the employer side:

- Social Insurance (SI): 17.5 percent of contractual salary, covering sickness, maternity, occupational accidents, retirement, and survivorship.

- Health Insurance (HI): 3 percent of contractual salary.

- Unemployment Insurance (UI): 1 percent of contractual salary.

The schedule is set by Decision 595/QD-BHXH and updated through Decree 58/2020/ND-CP. Contributions are capped at 20 times the regional minimum wage for SI and HI, which matters for senior roles where the cap binds.

On the employee side, an additional 10.5 percent is withheld for SI, HI, and UI combined. Personal Income Tax is withheld separately under Circular 111/2013/TT-BTC, at progressive rates from 5 to 35 percent.

Worked example: same senior backend role, Vietnam vs Netherlands

A senior backend engineer in Ho Chi Minh City or Hanoi typically commands USD 35,000 to USD 48,000 base salary in 2026, according to the Robert Walters Vietnam Salary Survey. Using USD 42,000 as the midpoint and the same six-step formula:

| Cost component | Amount (USD) | % of total |

|---|---|---|

| Base salary | 42,000 | 67% |

| Statutory contributions (21.5%) | 9,030 | 14% |

| 13th month accrual | 3,500 | 6% |

| Benefits (8%) | 3,360 | 5% |

| Onboarding amortised | 1,500 | 2% |

| Indirect overhead | 3,800 | 6% |

| Fully loaded total | 63,190 | 100% |

The same seniority role in the Netherlands lands at EUR 109,000 (roughly USD 118,000 at 2026 rates). The Vietnam fully loaded number is 46 percent lower for the same technical seniority, without compromising on candidate level when the hiring channel is set up correctly.

The 13th month accrual is a Vietnam-specific line that European budgets routinely miss. It is not legally mandatory under the Labor Code 2019, but it is so widely paid that omitting it from offers makes a role uncompetitive in the local market.

Entity setup vs EOR: how the cost model changes

Two paths exist to employ in Vietnam: set up a local entity, or use an EOR provider. The cost model differs in three ways.

| Factor | Entity setup | EOR |

|---|---|---|

| Timeline to first hire | 4 to 9 months | 5 to 14 days |

| Setup cost | USD 15,000 to USD 30,000 | None (per-employee fee only) |

| Ongoing legal and accounting | USD 800 to USD 2,500 monthly | Included in EOR fee |

| Per-employee fee on top of loaded cost | None | 10 to 15% of loaded cost typically |

| Breakeven point | 8 to 12 FTEs and above | Under 8 to 12 FTEs |

The breakeven calculation depends on package design and the level of operational support needed. A 2025 market analysis by Dentons LuatViet found that EOR remains more cost-efficient under roughly 8 to 12 FTEs for most international companies entering Vietnam.

Above that threshold, entity setup amortises faster. Below it, EOR removes the upfront cost and shortens time-to-first-hire from months to weeks.

How Sunbytes helps international companies calculate and run Vietnam employee cost correctly

Getting employee cost right is an operational decision, not just a planning exercise. The gap between a projected fully loaded cost and the actual monthly payroll often appears in month three, after statutory contributions have been filed, the 13th month has accrued, and the benefits package has been administered across a distributed team.

Sunbytes is a Netherlands-based technology and workforce solutions company with deep Vietnam operations. We help international companies model fully loaded employee cost before hiring decisions are made, and we run the payroll, statutory contributions, and benefits that turn those models into actual payouts on the 25th of each month.

Our work for international employers is organised around three pillars.

- Payroll Services runs payroll for international companies hiring in Vietnam. We handle the 21.5 percent mandatory employer contributions, PIT withholding under progressive bands, 13th month accrual, and monthly reporting to social insurance authorities. Companies see their fully loaded cost in advance, with no surprises in month three.

- Accelerate Workforce Solutions covers the hiring model choice itself, EOR for fast market entry without entity setup, dedicated remote teams for sustained engineering capacity, and recruitment support for project-based work. Time-to-first-hire under our EOR: 14 days from signed agreement.

- Digital Transformation Solutions supports companies that build their Vietnam workforce around technology delivery, including software engineering, DevOps, QA, and AI integration teams. The cost model is built into how we scope and deliver.

Our tagline is Transform, Secure, Accelerate. The Accelerate pillar is where employee cost lives, and where the discipline of getting cost right in month one prevents the budget overruns that derail market entry in month nine.

5 ways to lower employee cost without lowering quality

Reducing employee cost without lowering quality requires moving cost between categories, not cutting it from one. The five levers below are ranked by how often they apply across European companies expanding into APAC.

1. Geographic arbitrage: hire the same skill in a lower-cost market

The biggest single lever. Vietnam, Poland, Portugal, and Mexico all offer technical talent at 40 to 60 percent lower fully loaded cost than the Netherlands, UK, or Germany for equivalent technical seniority. The risk is integration cost, which a well-run EOR or dedicated team model absorbs.

2. Benefit restructuring: cash equivalent to tax-efficient package

In Vietnam, certain non-cash benefits (meal allowance up to VND 730,000 monthly, phone allowance, business uniform) are tax-deductible to the employer and tax-free to the employee within statutory caps. Reallocating part of base salary to these categories reduces total cost by 3 to 6 percent without reducing take-home for the employee.

3. Remote and hybrid: reduce workspace and equipment overhead

Full-remote models cut indirect overhead from 8 to 15 percent of base down to 6 to 10 percent. Hybrid models capture roughly half the savings while keeping office presence. The cost saving is real, but it only holds if remote operational discipline (async-first workflow, documented decisions) is in place.

4. Employment model: when EOR or contractor structures lower total cost

For under 8 to 12 FTEs in a new market, EOR is consistently cheaper than entity setup. For project-based work under 6 months, a properly classified contractor relationship avoids statutory burden. The misclassification risk in Vietnam is real, so the contractor route only works for genuinely independent engagements.

5. Onboarding standardization: cut amortised onboarding by 30 to 50 percent

Standardised 90-day onboarding (documented playbook, structured ramp milestones, pre-built first projects) cuts time-to-productivity from 4 to 6 months down to 2 to 3 months. According to SHRM Talent Acquisition Benchmark data, every month of ramp acceleration is worth roughly 8 percent of annual cost.

For under 8 to 12 full-time employees, EOR is consistently cheaper than entity setup once timeline, setup cost, and ongoing legal and accounting overhead are added in. Above that threshold, entity setup amortises faster and becomes the lower-cost option. The breakeven depends on benefit design, expected growth rate, and how much operational support the company needs from a local partner.

FAQs

On average, an employee costs 25 to 40 percent on top of their base salary in developed markets. The figure is higher in Western Europe, where statutory employer contributions and mandatory benefits can push the total to 50 percent above base. It is lower in markets with leaner statutory frameworks. In Vietnam, the additional cost above base is approximately 30 to 35 percent once SI, HI, UI, 13th month, and basic benefits are added.

Fully loaded employee cost equals base salary plus employer statutory contributions plus mandatory and competitive benefits plus amortised onboarding cost plus indirect overhead. The six-step version is laid out in the body of this article, with worked examples for the US, Netherlands, and Vietnam.

Salary is one of four cost categories the employer pays. The other three (statutory contributions, benefits, and indirect overhead) typically add 25 to 45 percent on top of base. They appear on different parts of the budget, which is why companies that budget against base salary alone routinely miss their headcount cost forecast in year one.

The SHRM Talent Acquisition Benchmark puts the average cost per hire at approximately USD 4,700 across industries. Technical and specialist roles run two to three times higher when agency fees, time-to-fill, and ramp time are included. This sits separately from the fully loaded cost calculation; it amortises into the onboarding line of the formula.

For under 8 to 12 full-time employees, EOR is consistently cheaper than entity setup once timeline, setup cost, and ongoing legal and accounting overhead are added in. Above that threshold, entity setup amortises faster and becomes the lower-cost option. The breakeven depends on benefit design, expected growth rate, and how much operational support the company needs from a local partner.

Let’s start with Sunbytes

Let us know your requirements for the team and we will contact you right away.