Your first Vietnam hire can look affordable on salary alone. Then finance asks the harder question. Should your company employ that person through an Employer of Record, or should it set up a Vietnamese entity first?

Employer of record ROI is the financial return from using an EOR instead of creating and running a local entity. In Vietnam, the calculation should compare EOR provider fees with entity setup cost, monthly local overhead, payroll ownership, SHUI and PIT administration, setup delay, and the value of getting a compliant hire started earlier.

For Dutch and EU companies planning 1 to 20 Vietnam hires, the ROI question is not only monthly fee versus monthly fee. The better question is: at this headcount and time horizon, which route creates less cost, less delay, and fewer clean-up issues?

If you are still evaluating the fundamentals of the employment model, start with this guide to EOR in Vietnam before building a financial comparison.

TL;DR

Employer of Record ROI in Vietnam is the cost advantage of using an EOR instead of setting up a local entity. EOR usually produces stronger ROI when avoided entity setup cost, avoided monthly overhead, and faster hiring value are higher than the EOR provider fees. Entity setup may win when Vietnam headcount is stable enough for annual EOR fees to exceed local entity fixed costs.

- Use this EOR vs entity cost model: shared employment costs + EOR-only costs + entity-only costs + setup delay cost + compliance ownership.

- EOR is usually stronger for the first 1 to 10 Vietnam employees, market testing, or uncertain long-term headcount.

- Entity setup may become financially stronger when Vietnam becomes a permanent base with larger headcount and local HR, payroll, finance, and legal support.

Best fit when: your company needs the first Vietnam hire active in weeks, not after a full entity setup process.

Watch out for: salary, SHUI, PIT, bonuses, and work tools are not automatic EOR savings because these costs may exist in both routes.

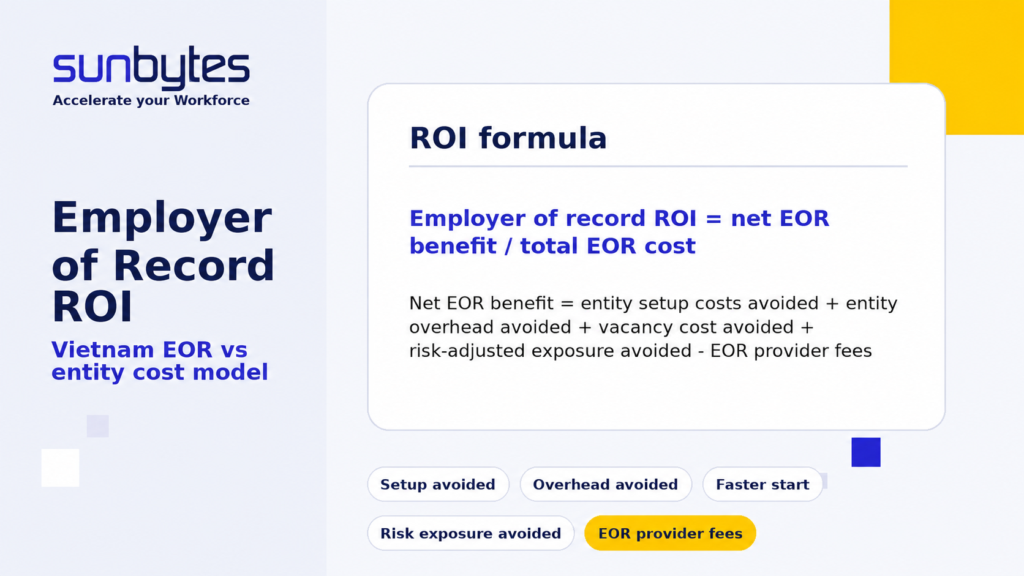

What employer of record ROI means

Employer of record ROI means the net financial benefit of using an Employer of Record compared with setting up and running your own local entity.

For a finance team, the simplest formula is:

Net EOR benefit = entity setup costs avoided + entity overhead avoided + vacancy cost avoided + risk-adjusted exposure avoided – EOR provider fees

The result can then be compared with the full cost of the EOR route over the same period.

A basic ROI version looks like this:

Employer of record ROI = net EOR benefit / total EOR cost

This model works only when the comparison is clean. Salary should not be counted as a saving if the employee receives the same salary in both routes. SHUI and PIT should not be counted as avoided costs if they still apply in both routes.

The difference usually sits in fixed cost, admin ownership, setup time, and the cost of fixing problems later.

What costs belong in an EOR ROI model in Vietnam

A Vietnam EOR ROI model should separate shared employment costs from route-specific costs.

Salary, employer statutory contributions, bonus policy, work equipment, and some work permit support may exist in both routes. EOR fees and provider onboarding fees sit on the EOR side. Entity incorporation, legal support, accounting, payroll administration, local HR ownership, and corporate maintenance sit on the entity side.

According to PwC Worldwide Tax Summaries – Vietnam, employer social insurance, health insurance, and unemployment insurance obligations should be included in workforce cost planning. A common planning assumption is 21.5% employer contribution before applicable caps and exceptions.

For a deeper breakdown of recurring and one-time expenses, review this guide on EOR cost in Vietnam alongside your ROI model.

| Cost input | EOR route | Entity route | ROI note |

|---|---|---|---|

| Gross salary | Include | Include | Shared baseline, not an EOR saving |

| Employer SHUI planning assumption | Include | Include | Shared baseline if employment setup is comparable |

| EOR management fee | Include | Exclude | Main recurring EOR-specific cost |

| EOR setup or onboarding fee | Include if charged | Exclude | One-time EOR-specific cost |

| Work permit support | Include if needed | Include if needed | Depends on employee nationality and role |

| 13th month or bonus policy | Include if offered | Include if offered | Include if part of the employment package |

| Entity setup cost | Exclude | Include | Fixed cost avoided by EOR |

| Monthly accounting and payroll | Exclude or reduce | Include | Entity overhead avoided or reduced by EOR |

| Legal and corporate maintenance | Exclude or reduce | Include | Entity overhead avoided or reduced by EOR |

| Local HR administration | Lower internal load | Higher internal load | Depends on your operating model |

| Office and admin overhead | Include if needed | Include if needed | Include only when required by the model |

| Vacancy or opportunity cost | Lower if start is faster | Higher if setup delays hiring | Often a major year-one difference |

A weak model treats the EOR fee as the full cost of the EOR route and treats entity setup as only a one-time registration cost. That makes the entity route look cleaner than it is.

A stronger model asks who owns payroll, who stores employee records, who updates statutory assumptions, who prepares employment documents, and who handles offboarding if the role ends.

Before estimating your break-even point, it also helps to understand how providers structure fees in this overview of EOR pricing Vietnam.

EOR vs entity setup cost: what changes in year one

Year one is where the EOR route often has its strongest financial case.

With EOR, the main cost is the recurring provider fee plus any setup or onboarding fee. With entity setup, cost starts before the first employee can be hired. Your company may need incorporation support, licensing, a registered address, legal review, accounting setup, payroll registration, bank account setup, tax setup, and ongoing local administration.

A foreign-owned company setup process can take several months depending on structure and licensing requirements. In Vietnam’s Labour Code, available through ILO NATLEX, defines employment relationships based on paid work, agreement, management, and supervision. This is one reason informal hiring arrangements are not a reliable substitute for compliant employment structures.

| Cost category | EOR route | Entity route | ROI implication |

|---|---|---|---|

| Salary | Paid through EOR payroll | Paid through local payroll | Usually neutral |

| Statutory employer costs | Managed through EOR process | Managed by entity payroll team | Usually neutral, but admin ownership differs |

| Setup time | 2 to 4 weeks as Sunbytes planning timeline | 3 to 6 months as conservative planning range | Faster start can reduce vacancy cost |

| Provider fee | Recurring EOR fee | Not applicable | Main EOR cost to test against fixed entity overhead |

| Legal entity setup | Not required for first hires | Required before direct local employment | Entity fixed cost is avoided by EOR |

| Local accounting and payroll | Included or coordinated through provider scope | Owned by your entity | Entity overhead grows beyond setup |

| Compliance ownership | Provider supports employment administration | Your local entity owns the process | The risk model changes, not only the cost model |

| Exit and offboarding | Provider-supported if in scope | Local HR or legal process required | Include exit admin in total cost |

The year-one model should use the hiring-ready date, not only the entity registration date. Payroll, employment documentation, data handling, and local administration must be ready before the route is useful.

Need to prove whether EOR is still the right route?

Sunbytes can help turn your Vietnam hiring plan into a finance-ready EOR vs entity model. Salary, SHUI, provider fees, setup timing, payroll ownership, employee data handling, and offboarding scope are visible before the offer is approved.

When EOR ROI is strongest

EOR ROI is usually strongest when speed, uncertainty, and fixed-cost avoidance matter more than long-term local control.

This often happens in four hiring situations:

First, your company is hiring its first 1 to 10 employees in Vietnam. Entity setup creates fixed cost before you know whether Vietnam should become a long-term base. EOR lets your first hires start while finance keeps the entity question open.

Second, your company is testing a role, market, or delivery function. A support hire, engineer, operations specialist, or country coordinator may prove the case for Vietnam. If the role changes after six months, entity setup may have created cost before the model was validated.

Third, your hiring timeline is shorter than your entity timeline. A candidate who can start next month may not wait for a 3 to 6 month setup plan. EOR onboarding in 2 to 4 weeks can preserve the hire while the long-term structure is still being assessed.

Fourth, your internal team does not yet have Vietnam payroll, SHUI, PIT, employment document, and offboarding ownership. EOR does not remove the need for compliance. EOR changes who runs the process and who keeps the records organised.

When entity setup may win financially

Entity setup may become financially stronger when Vietnam becomes a permanent operating base with stable headcount and enough local overhead to justify the fixed cost.

The break point is not one universal number. The break point depends on monthly EOR fee per employee, entity setup cost, local accounting cost, legal maintenance, internal HR capacity, payroll tooling, time horizon, and expected headcount.

Entity setup deserves serious review when your company expects a stable long-term Vietnam team, monthly EOR fees exceed local entity overhead, or direct local contracts and licences become part of the operating model.

Entity setup also becomes more practical when your company already has local HR, payroll, finance, and legal support.

If you are weighing both structures side by side, this comparison of EOR vs entity setup Vietnam provides a broader operational view beyond ROI alone.

A useful finance rule: EOR is often the stronger starting route. Entity setup becomes easier to defend when team size and permanence are clear enough to spread fixed cost across more employees.

How to calculate your EOR break-even point

The EOR break-even point is the headcount or time horizon where entity setup becomes cheaper than continued EOR use.

Use this planning formula:

Break-even headcount = annual entity fixed cost / annual EOR fee per employee

Then adjust the result for setup delay and compliance exposure.

A more useful finance model is:

Adjusted break-even headcount = annual entity fixed cost + setup delay cost + risk-adjusted exposure / annual EOR fee per employee

Example planning model, not Sunbytes pricing

| Input | Sample value |

|---|---|

| Annual entity fixed cost | EUR 48,000 |

| Annual EOR fee per employee | EUR 6,000 |

| Estimated setup delay cost | EUR 12,000 |

| Risk-adjusted exposure assumption | EUR 6,000 |

Basic break-even headcount:

EUR 48,000 / EUR 6,000 = 8 employees

Adjusted break-even headcount:

(EUR 48,000 + EUR 12,000 + EUR 6,000) / EUR 6,000 = 11 employees

In this sample, entity setup starts to look financially stronger around 8 employees on a pure fixed-cost model. The break-even point moves closer to 11 employees when setup delay and risk exposure are included.

The time horizon changes the answer. At 12 months, EOR may still win because entity setup absorbs too much of year-one budget. At 36 months, entity setup may win if headcount is stable and local overhead is controlled.

What compliance variables change the ROI model

Compliance belongs inside the ROI model because it changes the cost of each route.

In Vietnam, payroll ROI depends on more than salary payment. The employment model must account for labour contract structure, SHUI contribution treatment, PIT withholding, employee records, work permit checks for foreign workers, and personal data handling.

According to PwC Worldwide Tax Summaries – Vietnam Personal Income Tax, tax residents and non-residents are subject to different PIT rules, which can affect payroll administration and workforce planning.

The European Data Protection Board (EDPB) provides guidance on international personal data transfers under GDPR. This is relevant when employee records move between the EU and Vietnam.

Vietnam’s Personal Data Protection Law should also be reviewed when handling employee information. Businesses should monitor updates through official government publications and legal advisors to ensure compliance.

A low monthly fee can become expensive if your HR lead later has to chase unsigned contracts, unclear payroll files, missing employee records, or incomplete exit documents.

Before selecting a provider, use this checklist to compare EOR providers in Vietnam and identify differences in compliance ownership, payroll support, and employee administration.

How Sunbytes helps make the ROI visible before hiring

The ROI question is bigger than the monthly EOR fee. Your first Vietnam hire needs a signed employment route, a payroll owner, SHUI and PIT handling, employee records, and an offboarding process before a problem appears. The route should be clear before the offer is approved.

Sunbytes helps Dutch and EU companies compare EOR and entity setup before the hiring route is locked. The model covers salary, statutory employer costs, provider fee, onboarding timeline, payroll ownership, employee data handling, and offboarding scope.

EOR onboarding can run in 2 to 4 weeks. Payroll runs on time. Offboarding actions are handled within 24 hours when inputs are complete. The setup is supported by a Netherlands HQ, Vietnam delivery hub, and 4 to 5 hour NL-VN working overlap.

Finance gets a cleaner approval path. Your team can see which costs exist in both routes, which costs belong only to EOR, which costs belong only to entity setup, and where the break-even point may sit across 12, 24, and 36 months.

Ready to build a finance-ready hiring model? Calculate your EOR ROI with Sunbytes before committing to either route.

FAQs

Employer of record ROI is calculated by comparing the net financial benefit of EOR against the total EOR cost. The model should include entity setup costs avoided, entity overhead avoided, vacancy cost avoided, and risk-adjusted exposure avoided, minus EOR provider fees. For Vietnam, salary and statutory employer costs should usually be treated as shared baseline costs.

EOR is often financially stronger for early hires, small teams, and market testing. Entity setup may become cheaper at larger stable headcount, especially when your company has enough local HR, payroll, finance, and legal support to absorb fixed overhead. The right answer depends on headcount, time horizon, setup cost, and operating model.

Salary should usually be excluded from EOR savings if the employee receives the same salary in both routes. Statutory employer contributions should also be treated carefully because they may apply under both models. EOR savings usually come from avoided fixed setup cost, lower local overhead, faster start, and reduced admin clean-up.

There is no universal break-even headcount. A basic model is annual entity fixed cost divided by annual EOR fee per employee. A stronger model adjusts that number for setup delay, compliance exposure, local overhead, and the time horizon of the Vietnam hiring plan.

Employer of record ROI should include compliance risk as a risk-adjusted assumption. Weak employment setup can create later cost through payroll correction, missing records, unclear responsibility, or offboarding friction. Legal and tax penalty assumptions should be reviewed by qualified advisors before the model is used for board approval.

A company should review entity setup when Vietnam becomes a permanent base, headcount is stable, and entity overhead is lower than ongoing EOR fees. The decision should also consider whether the company needs direct local contracts, licences, office presence, or deeper local management control.

An EOR can support payroll administration, employment documentation, and statutory contribution handling within the agreed service scope. PIT and SHUI treatment still depends on employee profile, contract type, tax residence, contribution caps, and current law. Companies should review local requirements and provider responsibilities before onboarding employees in Vietnam.

Let’s start with Sunbytes

Let us know your requirements for the team and we will contact you right away.