Payroll migration is rarely planned from the start. Most businesses begin asking how to migrate payroll only after a trigger: an audit flags six months of withholding errors, an acquisition requires consolidated payroll reporting your current system cannot produce, or a new market operation needs a provider with local statutory capability your existing setup lacks. By the time the payroll migration decision is made, the risk is already accumulating.

TL;DR

- Payroll migration moves your payroll data, processes, and compliance obligations from one system or provider to another. It is not the same as a system upgrade within the same vendor. The four triggers that typically force the decision are compliance failure, system limitation, company restructure, and new market entry without adequate local payroll infrastructure.

- The 8-step process in this guide covers data audit, scope definition, field mapping, configuration, parallel-run validation, sign-off, and formal close-out. The parallel-run period is the most commonly skipped step.

- The remediation and penalty exposure for the pre-migration period cost more than two years of managed payroll fees. Migration cost is always lower than the accumulated liability it replaces.

What is payroll migration and when does your business need it?

“Payroll migration means transferring employment and payroll data, configuration, and compliance obligations from one system or provider to a new one.”

Most companies encounter this decision at least once, whether at a new market entry, during rapid headcount growth, or after a compliance review reveals that their current setup cannot meet the statutory requirements of the markets they operate in.

The payroll services available to international companies cover the full migration process, including data transfer, statutory re-registration, and the parallel-run period required to validate outputs before go-live.

4 triggers that signal your business needs to migrate payroll

- Compliance failure

An audit or inspection identifies systematic errors: incorrect withholding calculations, incomplete social insurance contributions, or reporting formats that do not meet statutory requirements. Your current system or provider cannot correct these at the process level. Patching individual errors does not solve the structural problem.

- System limitation

Your current payroll system cannot handle the reporting requirements your business now faces. This includes multi-currency payroll for foreign employees, statutory benefit calculations that vary by jurisdiction, or regulated reporting formats that require structured data fields your system does not support.

- Company restructure

An acquisition, merger, or entity change means two payroll systems must consolidate, or a new entity must be set up from scratch with compliant payroll infrastructure from day one.

- New market entry

Your company begins hiring in a new country using an in-house spreadsheet or a global platform without jurisdiction-specific statutory configuration. As headcount grows past ten employees, the compliance exposure of an unconfigured system becomes material.

What a payroll migration project covers and what it does not

A payroll migration project covers: employee master data transfer, pay element and earning code mapping, historical payroll record transfer for continuity of statutory calculations, configuration of the new system or provider, and re-registration of employees with relevant authorities where applicable.

These must be addressed as a separate remediation project before or alongside migration. It also does not cover HR system migration, changes to employment contracts, or benefits platform transitions. Defining these boundaries clearly at the start prevents scope creep that extends your timeline and concentrates risk.

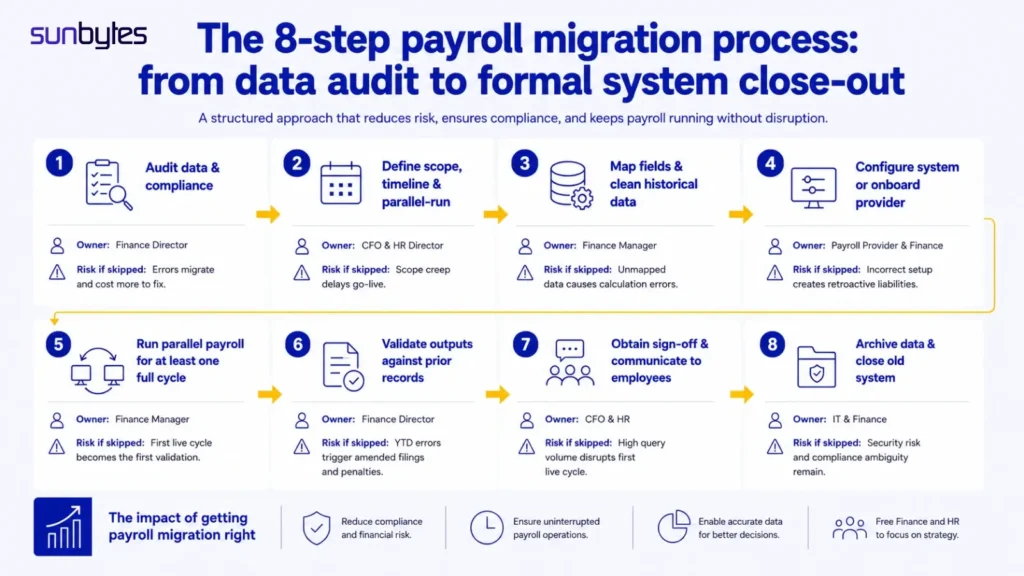

How to migrate payroll: a step-by-step guide (8 steps)

Understanding how to migrate payroll to a new provider starts with the 8 payroll system migration steps below. They apply regardless of your current system type or destination provider. Each step has a clear owner and a specific consequence if skipped. The parallel-run period in step 5 is the most critical and the most commonly omitted.

Before beginning, confirm that your new system or provider is correctly configured for the statutory requirements of every market in your scope. Reviewing payroll compliance for FDI businesses and your payroll processing guide for each relevant jurisdiction before migration starts prevents configuration errors from entering the live payroll cycle.

Step 1: Audit your current payroll data and compliance status

Before moving any data, understand exactly what you are moving. The audit covers: employee master data completeness and accuracy, payroll history for the previous 12 months minimum, statutory registration status for all employees, withholding records against submitted returns, and any open queries or discrepancies from prior cycles.

Owner: Finance Director and current payroll provider.

Risk if skipped: Errors in the source system migrate directly into the new one. Clean-up cost at destination is significantly higher than at source.

Step 2: Define migration scope, timeline, and parallel-run period

Scope defines what transfers: employee records, historical payroll data, pay element mapping, and payment configurations. Your timeline must include a non-negotiable parallel-run window of at least one full payroll cycle before go-live. Companies that skip this window have no pre-go-live validation mechanism.

Owner: CFO and HR Director.

Risk if skipped: Without defined scope, the migration expands during execution. Each addition extends the timeline and introduces new validation requirements.

Step 3: Map data fields and clean historical payroll records

Data mapping translates the field structure of your old system into the structure of the new one. Pay elements, earning codes, deduction categories, and allowance classifications all need explicit mapping decisions. This step also identifies records that are incomplete, duplicated, or formatted inconsistently.

Owner: Finance Manager and new payroll provider.

Risk if skipped: Unmapped fields default to zero or null in the new system, producing calculation errors on the first live cycle.

Step 4: Configure the new system or onboard the new provider

Configuration includes: statutory contribution calculation bases for each jurisdiction you operate in, withholding tables for all employee types, regulatory reporting template setup, and payment file formats compatible with your banking arrangements. For a managed provider, this step also includes executing the service agreement and completing any statutory registration transfers.

Owner: New payroll provider and Finance.

Risk if skipped: A system not configured for the statutory rules of your markets will produce incorrect outputs from the first cycle. These become retroactive liabilities if not caught before go-live.

Step 5: Run parallel payroll for at least one full cycle

Parallel payroll means processing the same pay period through both the old and new systems independently, then comparing outputs line by line. This is the validation mechanism that catches configuration errors, mapping failures, and calculation differences before they reach employees or authorities.

Owner: Finance Manager.

Risk if skipped: This is the step most commonly omitted under time pressure. Without it, your first live cycle is also your first validation cycle, with no fallback and no prior-system comparison available.

Step 6: Validate all outputs against prior payroll records

Validation goes beyond the parallel-run comparison. It confirms that cumulative year-to-date figures are transferred correctly, that statutory contribution bases are consistent with the prior system, that withholding calculations match your authority submissions for the current year, and that all deduction and benefit calculations carry over correctly.

Owner: Finance Director and payroll provider.

Risk if skipped: Year-to-date errors discovered after go-live require corrections across multiple historical cycles, triggering amended filings and potential penalty interest.

Step 7: Obtain Finance sign-off and communicate changes to employees

Finance sign-off confirms that the parallel-run results are acceptable and the new system is authorised for live operation. Employee communication covers: any changes to payslip format, timing of the first payment from the new system, point of contact for payroll queries, and confirmation that bank account details have been verified.

Owner: CFO and HR.

Risk if skipped: Employees who receive their first payslip from a new system without prior communication generate high-volume query traffic that disrupts payroll operations in your first live cycle.

Step 8: Archive legacy data and formally close the old system

Legacy payroll data must be archived in a format accessible for audit purposes for the retention period required by each jurisdiction you operate in. The old system is formally decommissioned only after archive confirmation. All access credentials and API connections to third-party systems must be revoked.

Owner: IT and Finance.

Risk if skipped: An unclosed legacy system creates a data security risk and a compliance ambiguity. If both systems hold employee records, the authoritative source is undefined.

Payroll migration risks: what goes wrong and how to prevent it

The three highest-impact risks in a payroll migration project can each be prevented at the planning stage. The table below shows what each risk looks like, when it typically surfaces, and what prevents it.

| Risk | When it surfaces | Financial consequence | Prevention |

|---|---|---|---|

| Data integrity failure | First live payroll cycle | Calculation errors requiring retroactive correction across all affected cycles | Data audit in step 1 + field mapping sign-off in step 3 |

| Skipping parallel-run | First live cycle, no fallback | Errors discovered after old system is closed, no comparison data available | Non-negotiable parallel-run period in step 5 |

| Compliance timing gap | End of first month after go-live | Late contribution filings attracting daily penalty interest from day one of delay | Written handover protocol assigning responsibility per obligation before transfer |

Most payroll migration failures are not caused by the migration itself. They are caused by what was already wrong with your source system, combined with insufficient validation before go-live.

Data integrity failures during payroll migration

The most common data integrity failure is migrating corrupted or incomplete records without detecting them first. Historical payroll data accumulated in spreadsheets typically contains formatting inconsistencies, blank fields, and calculation overrides that do not translate correctly into a structured system.

The second failure type is field mapping that silently drops data. When your source system has a field for “housing allowance” and the destination maps it to “other allowance” without documentation, the statutory contribution base changes. The change is invisible in the payslip but alters every statutory calculation and creates retroactive exposure from the first affected cycle.

Employee data transferred during migration is subject to applicable personal data protection obligations in each jurisdiction. In the EU, GDPR Article 46 applies to cross-border transfers. Data transferred to a new provider constitutes a disclosure of personal data and requires a documented legal basis. Review your CyberSecurity Solutions and managed security service options before initiating any data transfer to ensure your data handling meets applicable requirements.

Compliance gaps created by poor migration timing

Your payroll compliance obligations do not pause during a migration. Statutory contributions are due on fixed dates. Withholding must be deducted from every salary payment. Regulatory reports file on mandatory schedules. A migration that straddles a reporting deadline without a clear handover protocol creates gaps in these obligations.

The most common timing failure is a provider change that takes effect on the first of the month, but where statutory registration with the new provider is not completed until the second week. Contributions for the first two weeks are then either late or filed by neither provider. In most jurisdictions, late statutory contributions attract penalty interest from the first day of delay.

Employee communication failures and how to prevent them

Employees who receive a payslip from an unfamiliar provider without prior notice generate immediate queries to your HR team. At volume, this floods HR during the most operationally demanding period of the migration: your first life cycle.

Communication should go out at least two weeks before the first live payslip, covering: the name of the new payroll provider, any change to payslip format, the date of the first payment under the new system, and who to contact with queries. Employees with housing or education subsidies processed through payroll should receive individual confirmation that their deductions have transferred correctly.

Payroll migration in Vietnam: compliance requirements during transition

The steps above apply in any market. If you are migrating payroll for operations in Vietnam, three statutory obligations require specific attention because they do not exist in the same form in European markets.

A full explanation of how Vietnamese tax applies to foreign employee compensation is in the guide to Vietnam tax system for foreign workers.

PIT and SHUI continuity requirements during a provider change

PIT withholding in Vietnam is calculated on a cumulative basis across the tax year. When an employee moves from one payroll provider to another mid-year, the new provider must receive accurate year-to-date income and withholding figures to continue the cumulative calculation correctly. A provider that starts from zero in month seven will under-withhold for the rest of the year, creating a tax shortfall the employee must settle at annual finalisation.

SHUI registration in Vietnam is with Vietnam Social Security at the provincial level. A provider change requires deregistration from the outgoing provider’s account, registration under the incoming provider’s account, and a transfer confirmation from VSS. The registration process typically takes 5 to 10 business days based on Sunbytes payroll migration engagements in Vietnam. The gap between deregistration and registration must not span a contribution due date.

MoLISA reporting obligations that must not lapse during migration

The monthly labor report and the semi-annual and annual labor utilisation reports under Vietnamese law remain the employer’s obligation regardless of which provider processes payroll. During migration, confirm which entity is responsible for each report during the transition period. A missed monthly report under Decree 12/2022/ND-CP carries an administrative penalty of VND 1,000,000 to VND 3,000,000 per occurrence.

Data handling and protection requirements under Vietnamese law

Employee personal data transferred between payroll providers is subject to Decree 13/2023/ND-CP on personal data protection. The transfer must be documented, the receiving provider must be named as a data processor, and employees must be informed. A Data Processing Agreement between your company and the new provider is required before any data transfer begins.

Payroll migration go-live checklist: what to verify before switching

Before closing the old system, Finance must confirm each item below. Completing this payroll migration checklist before go-live prevents errors that cost significantly more to correct after the migration is live.

A post-migration audit at the 90-day mark is strongly recommended. This connects directly to the practices covered in the guide to why your business needs regular payroll audits.

Data verification: what to confirm before go-live

Employee master data: Every active employee has a complete record in the new system, including all statutory identifiers, bank account, contribution history, and employment contract dates.

Pay element mapping: All earnings, allowances, and deductions have a confirmed equivalent in the new system. The mapping document has been signed off by Finance.

Year-to-date figures: Cumulative gross income, taxes withheld, and statutory contributions are consistent between the old system’s final output and the new system’s opening balances.

Bank payment configuration: Payment file format is tested and confirmed with your bank. A test payment of a nominal amount per employee is recommended before the first full payment run.

Parallel-run comparison: The parallel-run output has been reviewed line by line. All variances are documented and explained. Unexplained variances have been corrected in the new system before go-live.

Compliance verification: what Finance must sign off before go-live

Statutory registration: The new provider has completed all required registrations for employees with relevant authorities. Registration confirmation is on file. The effective date is the first day of the first payroll cycle under the new provider.

Withholding configuration: Tax tables and contribution calculation bases are correctly configured for every employee type and jurisdiction in scope.

Reporting continuity: The prior period’s regulatory reports have been filed by the outgoing provider. The new provider is confirmed to file from the current period forward. Reporting continuity is documented.

DPA executed: The Data Processing Agreement with the new provider has been signed before any employee data was transferred.

Parallel-run sign-off: Finance Director has signed the parallel-run verification document, confirming that outputs are acceptable and the new system is authorised for live operation.

If your current payroll has compliance gaps or is managed manually, Sunbytes handles payroll migration for international companies in Vietnam with a structured 8-week process: data audit, SHUI re-registration, parallel-run validation, and MoLISA reporting continuity.

Explore Accelerate Workforce Solutions

How Sunbytes manages payroll migration for international companies?

Sunbytes is a Dutch-founded technology and workforce company founded in 2011, with 300+ client projects across 20+ countries.

- Payroll infrastructure that handles compliance from day one.

Through Accelerate Workforce Solutions, Sunbytes provides managed payroll with SHUI and PIT handled in-house, MoLISA reporting managed directly, and a structured 8-week migration process including parallel-run validation and compliance verification at each step. Employment contracts issued within 48 hours. Payroll on time every cycle. Offboarding within 24 hours. ISO 27001 certified. Signed Data Processing Agreement on all engagements.

- Technical integration for payroll system connectivity.

For companies connecting payroll to a European HR or ERP system, Digital Transformation Solutions handles the integration architecture. Data flows are mapped before migration begins, not after go-live , the difference between a planned integration and an unplanned reconciliation problem.

- Data protection across the full migration lifecycle.

Employee data transferred during migration is subject to applicable data protection law in every jurisdiction involved. CyberSecurity Solutions embeds both GDPR and local data protection requirements into the migration process from the first data transfer, so the migration does not create a data liability alongside the payroll one.

FAQs

For a company with 20 to 100 employees, a well-structured payroll migration takes 6 to 10 weeks from data audit to first live payroll cycle across Sunbytes managed migrations 2024 to 2025. The primary variable is the condition of your source data. Clean, complete records with documented year-to-date figures compress the timeline. Spreadsheet-based payroll with gaps or formatting inconsistencies extends it.

The Dutch manufacturing company’s migration took 8 weeks. Pre-migration data remediation, addressing six months of withholding errors, ran in parallel and added two additional weeks to the overall project.

Minimum requirements: employee master records, payroll history for the previous 12 months, year-to-date gross income and taxes withheld for the current year, statutory contribution history by employee, and all active deduction and benefit configurations.

In jurisdictions where statutory audit exposure extends beyond 12 months, prepare a longer payroll history. In Vietnam, for example, a 36-month history is recommended because SHUI audit exposure can reach back three years under social insurance law.

The three highest-impact risks are: data integrity failure during transfer, skipping the parallel-run period, and compliance timing gaps during the provider handover. All three are preventable with a structured plan. None are recoverable without cost once your old system is closed.

Yes. One full payroll cycle is the minimum. Two cycles is the recommended standard, because the first parallel run typically surfaces configuration issues that require correction before the second run can confirm clean outputs. A parallel run that produces variances is not a failure , it is the mechanism working as intended.

Historical payroll data must be archived in a format accessible for audit purposes for the retention period required in each of your jurisdictions. The old system should be formally decommissioned only after archive confirmation is documented. The Data Processing Agreement with your new provider should specify retention periods, access rights, and deletion protocols.

Payroll migration in Vietnam involves three obligations specific to the Vietnamese statutory framework: SHUI registration transfer with VSS at the provincial level, PIT withholding continuity using cumulative calculation, and MoLISA labor report filing continuity during the handover. A managed provider with Vietnam entity ownership and in-house SHUI and PIT administration handles all three. Responsibility for each obligation during the transition must be assigned in writing before data transfer begins.

Let’s start with Sunbytes

Let us know your requirements for the team and we will contact you right away.